Personal Income Tax in Vietnam

Personal Income Tax (PIT) is withheld from the income earned by the employee in Vietnam from providing works under labor contract or agreement.

TAX RESIDENT STATUS

Tax residence status plays a key role in determining PIT applicable rate when calculation for taxpayer in Vietnam.

Tax resident is the individual residing in Vietnam more than 183 days or having house rental from 183-day term. Non-tax resident does not meet abovementioned condition.

PERIODICAL FILINGS

PIT is declared on monthly or quarterly basis. PIT return is prepared and submitted online to tax office accordingly.

Deadline for PIT periodical filings is no later than 20th date of next month or 30t date of the month following quarter, corresponding to monthly or quarterly basis respectively.

PIT APPLICABLE RATES

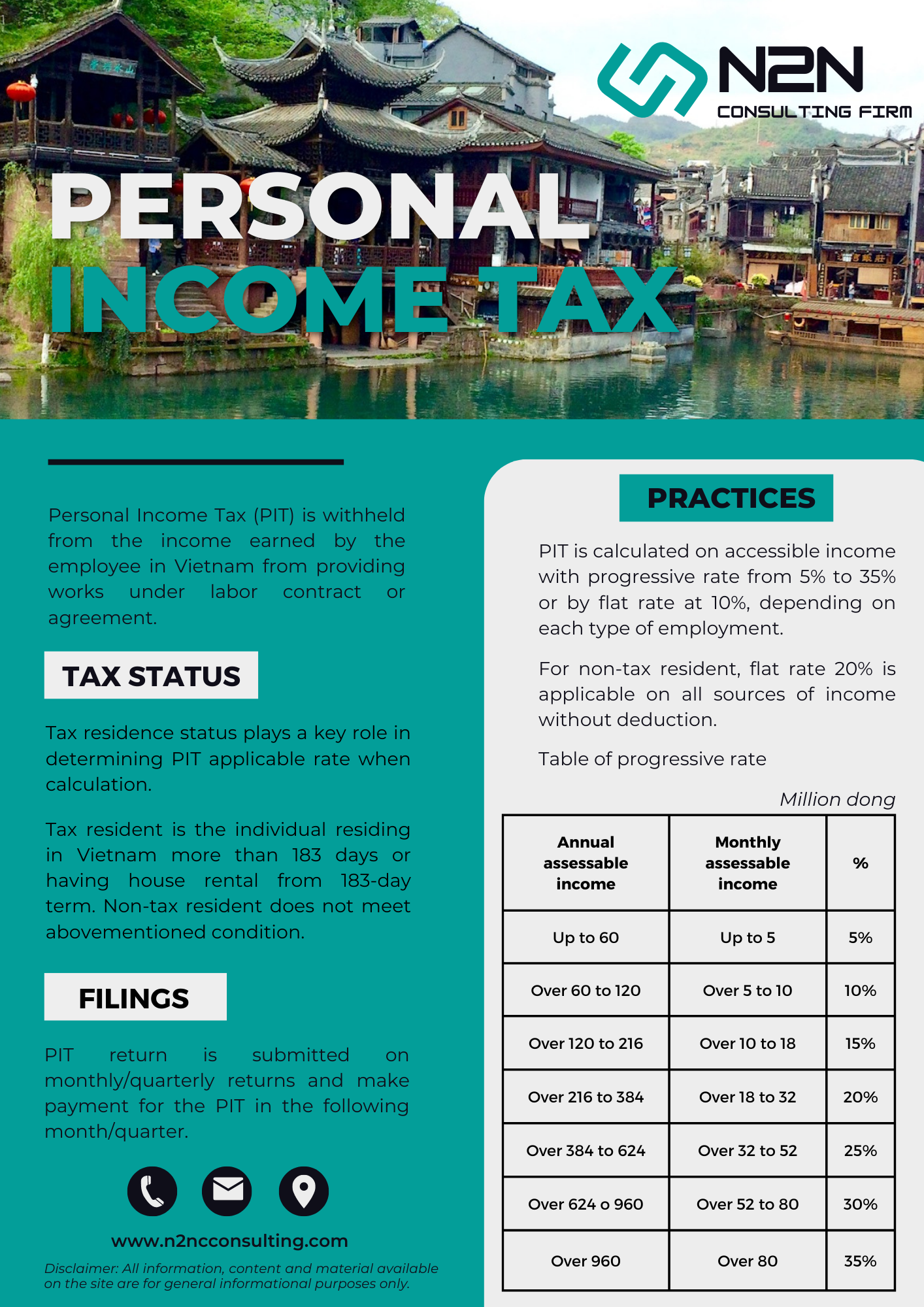

PIT is calculated on accessible income with progressive rate from 5% to 35% or by flat rate at 10%, depending on each type of employment.

For non-tax resident, flat rate 20% is applicable on all sources of income without deduction.

Table of PIT progressive rate

|

Unit: Million dong |

||

| Annual assessable income | Monthly assessable income | % |

| Up to 60 | Up to 5 | 5% |

| Over 60 to 120 | Over 5 to 10 | 10% |

| Over 120 to 216 | Over 10 to 18 | 15% |

| Over 216 to 384 | Over 18 to 32 | 20% |

| Over 384 to 624 | Over 32 to 52 | 25% |

| Over 624 o 960 | Over 52 to 80 | 30% |

| Over 960 | Over 80 | 35% |

{kind=link}